5 Budgeting Methods to Take Control of Your Money (Even If You Hate Spreadsheets)

10/12/20256 min read

Why It’s Effective

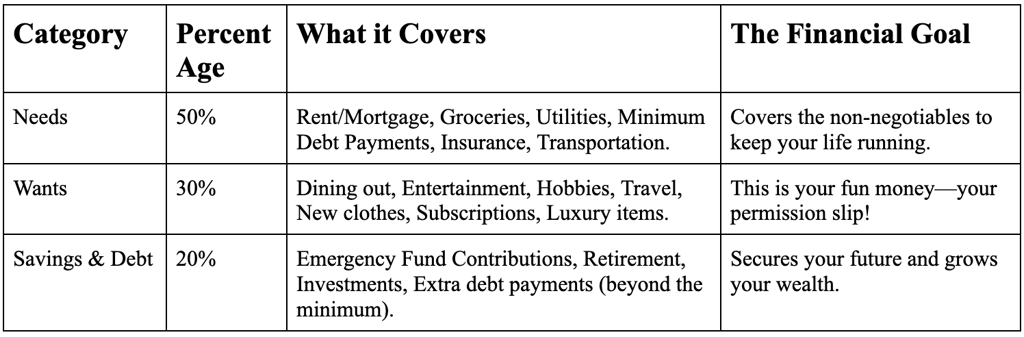

Low Friction: You only need to know three numbers, not 30.

Built-in Balance: It forces a healthy boundary between living in the present (30% Wants) and investing in the future (20% Savings).

Empathy-Focused: It acknowledges that having fun is necessary for a sustainable life.

Best Suited For:

People with stable incomes who value simplicity and don't have massive, complicated debt to manage.

2. The Debt-Crushing Method: Budgeting Backwards (For the Strategist)

If your main goal is to pay off high-interest debt (like credit cards or high student loans), the traditional 50/30/20 can feel too slow. This method prioritizes accelerated debt repayment above all else.

How It Works (The Science of Momentum)

This method flips the budgeting process by calculating your spending after you’ve secured your savings and debt payments.

Determine Target Savings: Decide how much you will save/invest first (e.g., $500).

Determine Target Debt Payment: Decide how much extra you will pay toward high-interest debt (e.g., $300 beyond the minimum).

Calculate Fixed Needs: Subtract your non-negotiable bills (rent, insurance, minimum debt) from what remains.

The Remainder is Your Spending: The very last remaining number is your "flexible spending allowance" for groceries, gas, and fun.

Why It’s Effective

Behavioral Economics: This method uses the power of the "Pay Yourself First" principle, which is a key tenet of wealth building. You treat savings and debt repayment as non-negotiable bills, which tricks your brain into prioritizing the future.

Clear Goal Orientation: It gives immediate, tangible satisfaction every time you make an extra debt payment, leveraging the reward system in your brain to keep you motivated.

Best Suited For:

Anyone whose financial goal is aggressively reducing debt or rapidly building an emergency fund.

3. The Hands-On Method: The Envelope System (For the Visual/Tactile Learner)

This is the classic, old-school method popularized by financial experts, but it's still extremely effective because it leverages the psychological pain of "real" money.

How It Works (The Science of Pain Points)

At the beginning of the month, you withdraw the cash for all your variable spending categories (groceries, dining out, entertainment) and place it into labeled envelopes.

When you buy groceries, you pay with the money from the "Groceries" envelope.

When the envelope is empty, that's it. You cannot spend in that category until the next month.

Why It’s Effective

The Pain of Cash: Research shows that paying with cash feels more psychologically painful than swiping a card. This natural reluctance to part with physical money forces you to be hyper-aware of every purchase, reducing impulse buys.

Zero-Based Budgeting: This method is a form of Zero-Based Budgeting (ZBB), where your income minus your expenses should equal zero. Every dollar is accounted for, eliminating that "Where did my money go?" mystery.

Sensory Cues: For visual or tactile learners who hate digital spreadsheets, the physical envelopes serve as immediate, unambiguous warnings.

Best Suited For:

People who frequently overspend with credit cards, who enjoy being hands-on, or who prefer a concrete, visual system over an abstract app.

4. The Anti-Budget Method: The Automated "Set It and Forget It" (For the Highly Disorganized)

If tracking expenses for 30 days sounds like torture, and you mainly struggle with discretionary spending, the Anti-Budget is your answer.

How It Works (The Science of Automation)

You automate your savings and investments first, and then you simply spend whatever is left over—no tracking required.

Determine Your "Freedom" Number: Decide on a non-negotiable percentage of your paycheck you want to save/invest (e.g., 30%).

Automate the Transfer: Set up an automatic transfer the day your paycheck lands. This 30% goes directly to a high-yield savings account or investment account before it ever hits your checking account.

Spend the Rest: Whatever is left in your checking account is your official spending money for the month—for needs, wants, and everything else. You don't have to track it, because you know your future is already secured.

Why It’s Effective

Eliminates Willpower: By automating the most important part (savings), you remove the need for willpower and daily tracking. The system works even if you forget about it.

Behavioral Constraint: This system creates a positive constraint. If you overspend on coffee, you run out of money sooner, naturally slowing your spending without guilt, because you know your most crucial financial goals are already met.

Best Suited For:

People who value convenience, travel often, or simply hate the administration of money management but are committed to saving.

5. The Detailed Method: Zero-Based Budgeting (For the Controller)

If you love the feeling of command and truly want to know where every single dollar goes, Zero-Based Budgeting (ZBB) is the most comprehensive and powerful approach. (The Envelope System is ZBB using cash, but this digital version allows for more complexity).

How It Works (The Science of Mindfulness)

At the beginning of the month, you budget until your Income minus Expenses equals zero ($0).

Forecast Income: Start by knowing exactly how much money you expect to receive.

List Fixed Expenses: Budget for all non-negotiables (Rent, Minimum Debt).

List Savings/Goals: Budget for your savings goals (Emergency Fund, New Car Fund).

Allocate Variable Spending: Allocate the remaining money into categories like Groceries, Gas, Fun, and Clothing.

Assign Every Dollar: If you have $50 left over, you must assign that $50 to a specific category (e.g., $25 to Fun, $25 to Buffer). Nothing is left unassigned.

Why It’s Effective

Financial Mindfulness: It forces you to be mindful of your money before you spend it, transforming you from a passive participant into an active manager.

Reduced Guilt: When you spend money in a category, you can do so guilt-free because you explicitly gave yourself permission to spend that exact amount.

Proactive Problem Solving: When a category runs low, you are forced to consciously "roll with the punches" (e.g., taking $50 from the "Clothing" budget and moving it to the "Groceries" budget), keeping you engaged and in control.

Best Suited For:

People with highly variable incomes, complex financial situations, or those who thrive on detailed information and tracking.

The Final Word: Start Where You Are

If you take anything away from this post, let it be this: Taking control of your money is a profound act of self-care. It reduces cortisol, decreases relationship tension, and grants you the ultimate freedom: the power of choice.

Don't start with the most complicated method (ZBB) if you are naturally disorganized. Instead, start with the simplest (50/30/20) or the most hands-on (Envelope System).

The "best" budgeting method is the one you will actually stick to, consistently. Choose a method, commit for 30 days, and watch your financial anxiety start to fade away.

If you'd like the perfect tool to make your entire budgeting process easier, make sure to grab my fully automated budgeting spreadsheet down below!

Based on your personality, which of these five methods feels like the most realistic and least intimidating way for you to start taking action today? I’d love to hear your thoughts down below!

5 Budgeting Methods to Take Control of Your Money (Even If You Hate Spreadsheets)

Let's be honest: when you hear the word "budget," what do you feel? If your answer is anxiety, restriction, or instant brain fog, you're definitely not alone.

Most people skip budgeting because they believe it requires a stressful, complicated spreadsheet, or worse, that it means you have to stop enjoying your life.

The truth is, budgeting isn't about cutting out lattes; it’s about giving every dollar a job so you stop worrying where it went. It’s a tool for financial self-worth—it puts you in the driver’s seat of your future.

If the spreadsheet method feels too overwhelming, you simply need a different strategy. We're going to dive into five proven budgeting methods, from the minimalist to the meticulously detailed, so you can find the one that works with your personality, not against it.

The Core Problem: Why We Resist Budgeting

Budgeting resistance is rooted in two psychological fears:

Fear of Scarcity: We worry that seeing the truth of our finances will confirm we don't have enough, triggering an urge to ignore the problem entirely.

Fear of Restriction: We equate a budget with rules that prevent us from having fun.

The solution is reframing: A budget is a permission slip to spend money on what truly matters to you, while intentionally diverting funds away from what doesn't.

1. The Simplest Method: The 50/30/20 Rule (For the Minimalist)

This method is perfect if you want a quick overview and don't want to track every penny. It’s based on a proportional split of your after-tax income.

How It Works (The Science of Simplicity)

The 50/30/20 rule minimizes the decision fatigue that causes most people to quit budgeting. Instead of choosing line items, you assign your entire paycheck into three large buckets:

If you’d like to continue this beautiful self journey, here are some more posts you'll love!

Get in touch!

Feel free to share your thoughts, tips, and posts/products you like to see!